Bangladesh has taken considerable steps to ensure UHC can be achieved by 2030, but it still remains an uphill battle.

The government’s low health spend, 2.8 per cent of its GDP – one of the smallest in the world, has led to substantial out-of-pocket (OOP) healthcare expenditures, rising from 55.9 per cent in 1997 to 67 per cent in 2015, now one of the highest in the world. Five million people are more vulnerable to poverty every year due to healthcare-related expenses, while 41.6 per cent seek services from informal healthcare providers, which can result in incompetent treatment and over-usage of medications.

Reducing dependency on OOP payments and developing a mechanism for adequate and quality access to services remains a priority for the government, hence the introduction of the Healthcare Financing Strategy 2012-2030 of Bangladesh.

It proposes to extend coverage while developing mechanisms for financing this initiative. The strategy identified 85.7 million people (approximately 56.2 per cent of the population) associated with the informal work sector. Despite the challenges of undertaking this endeavour, it is essential to include this target group in healthcare enterprises as informal workers comprise 88 per cent of the country’s labour force and contribute 64 per cent to the Bangladesh’s GDP.

The Strategy emphasised community-based health insurance and micro health insurance as social protection programmes for the informal sector population. These types of healthcare schemes are widely recognised as potential outlets for people in low-income brackets to gain access to the health system. One of the biggest hurdles in such schemes is enrollment – which is critical for its sustainability. However, a wide range of factors, including features of the benefit package, payment schedules, lack of awareness, and clients’ satisfaction can reduce enrollment and successful implementation of these health schemes.

icddr,b has conducted various studies testing variables relating to health insurance schemes, exploring, among other things, the reasons and motivation for enrollment, the demographic and geographical factors affecting enrollment and willingness to pay insurance, the likelihood of services sought, and user satisfaction and lessons learned from implementing a health insurance scheme.

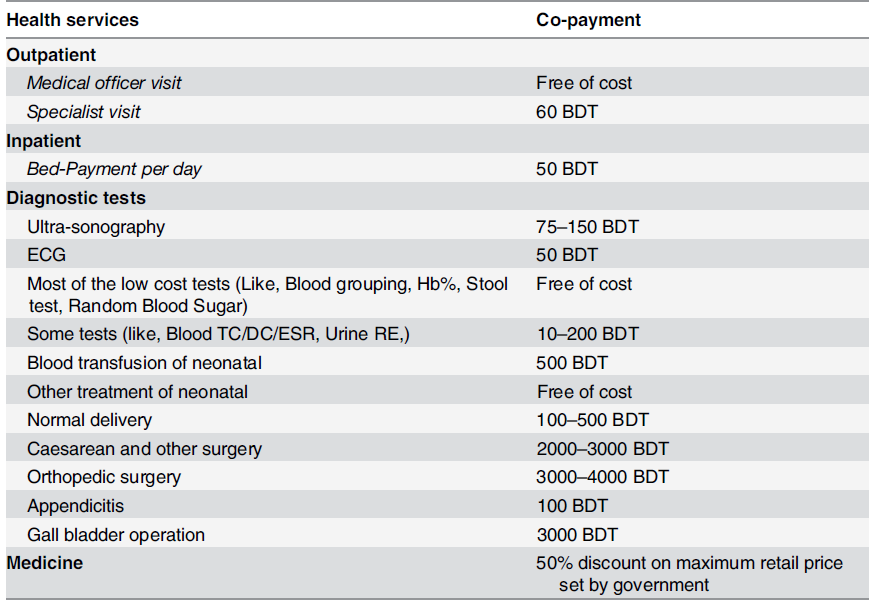

In a study of 557 informal workers in Dhaka, 86.7 per cent were willing to pay for a community-based health insurance scheme based on the benefit package akin to Gonoshasthaya Kendra (Table 1), with the option to pay premiums weekly or monthly (63.4 per cent chose the former). Moreover, workers with up to a primary level education (26.9 per cent) were less willing to pay for insurance than those who had less than one year of schooling. This denotes that educational level is important when considering enrollment as those who resided in sub-district and district areas were less likely to sign on for an insurance scheme than those who lived in the metropolitan area.

Table 1: The service package of the health insurance product. Source: Original study.

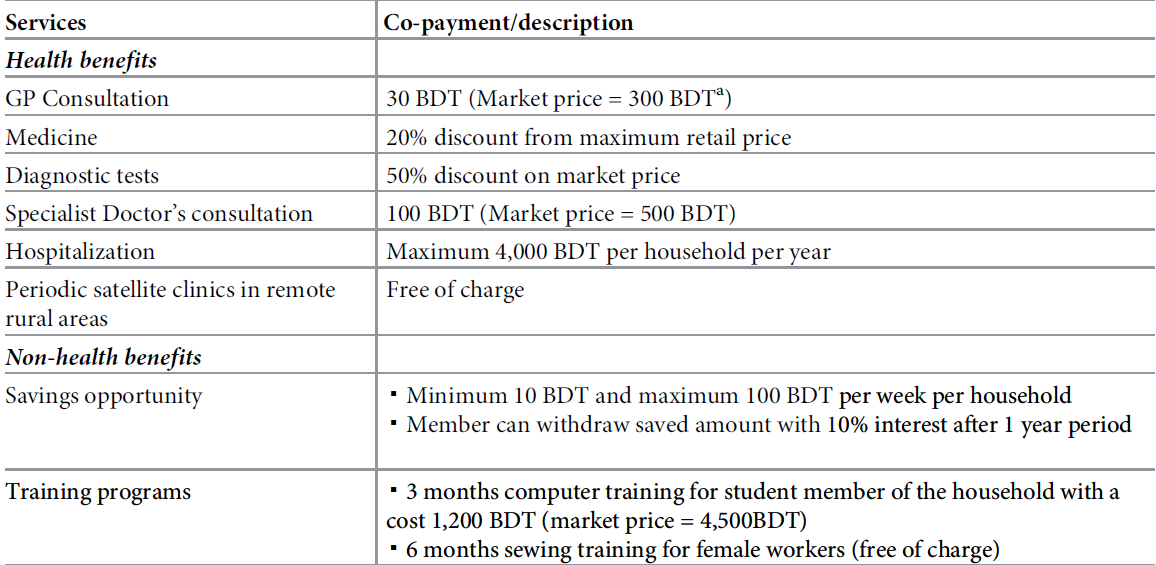

Based on the interesting results elicited from this study, icddr,b collaborated with the Labor Association for Social Protection (a cooperative under the Ministry of Local Government and Rural Development) on a pilot insurance scheme (Table 2) in Chandpur, Bangladesh, targeting low-income informal workers. The premium was set at BDT 600 (USD 7.72) per household per year (which accounts for 2.68 per cent of the annual income for these workers) and six members from each household were entitled to health benefits under one membership card.

Table 2: The service package of the community-based health insurance scheme. Source: Original study

Insured individuals were more likely than the uninsured to seek services from a medically trained provider (MTP) and less likely to visit a village doctor and drug seller by 12 per cent and three per cent respectively. One factor contributing to this statistic could be that healthcare from an MTP became more accessible (and affordable) once the informal workers enrolled in the insurance scheme.

A follow up study measured the beneficiaries’ satisfaction with the community-based health insurance scheme. Of the 233 young adults interviewed (aged 18-44), 60 per cent had some health issues, with 81.5 per cent (cumulative) were content with the services provided by the clinics they visited. Above all, an overwhelming majority (95 per cent) reported satisfaction with the self-financed health scheme.

Dr Jahangir Khan, the former head of the health economics unit of icddr,b, added that “community-based health insurance schemes should be implemented as an add-on project of existing organisations, like cooperatives, based on solidarity and economic interest in order to bring people under financial risk protection for health to achieve universal health coverage in Bangladesh”.

Aside from developing a community-based health insurance scheme, icddr,b also established a micro health insurance scheme in Chakaria, Bangladesh which enrolled households against a yearly premium. The benefit packages included outpatient care at village health posts (VHP, which are primary healthcare centres established jointly by community and icddr,b) as well as inpatient care at select hospitals and discounted prices on medicines and diagnostic tests. The scheme had a modest 20 per cent enrollment rate, but for any health insurance initiative to be successful, participation is required in large numbers to ensure effective risk pooling and to maintain an affordable premium for all.

Diving further, the researchers examined the determinants for enrollment and the factors preventing the majority from signing on to a scheme. A higher proportion of households from highest socioeconomic quintile enrolled into the scheme compared to lower socioeconomic quintile (56.2 per cent vs. 43.8 per cent). Enrollment was higher for households with main earners engaged in public/private services (64 per cent). Enrollees were also reasonably more financially literate (55.5 per cent enrollment among financially literate households) and more educated, with majority of households with main earner having more than 10 years of education joining the scheme (64.8 per cent).

Thus, it can be surmised that there is a direct correlation between education level and willingness to enroll in any health insurance scheme. The higher the education level of the primary earner, the more they are to be aware of the risks of ill health, the related financial shocks and the protection offered by such schemes. However, one of the biggest drawbacks for those unwilling to enroll relates to distance to the nearest health centres. Households which were situated in villages with a VHP were more inclined to join the scheme than those which did not (68 per cent vs 47 per cent).

Despite the evidence-based benefits of health insurance schemes, there remains a multitude of challenges in adopting such schemes in resource-poor settings. Insuring the population from healthcare related expenditures is a comparatively newer concept in Bangladesh, and there remains a mountain of challenges in protecting various disparate groups with different healthcare needs, socioeconomic levels, and willingness to engage in insurance schemes.

Additional variables can relate to age, education and literacy levels, household sizes and earning capability of the primary earner, access and availability of healthcare services, and most importantly affordability of the premiums. As the icddr,b studies have indicated, to target the financially disadvantaged and less educated, there needs to be more concerted effort to raise awareness on the cost-benefits of enrolling in health insurance schemes. This is particularly critical as this demographic represents the majority of Bangladesh’s population.

A large number of schemes in low and middle income countries charge a flat premium which puts the poor at a considerable disadvantage as they are the highest contributors compared to wealthier proportions of the population. One solution to this dilemma, as concluded by the studies, could be to design and offer mechanisms for safety-nets where premiums for the less wealthy are subsidised, reducing non-financial barriers and inequities for those in lower socioeconomic brackets. This would allow for more equity in the scheme. These factors should be considered when the government develops a social insurance scheme as part of its endeavours towards achieving universal health coverage.